Search

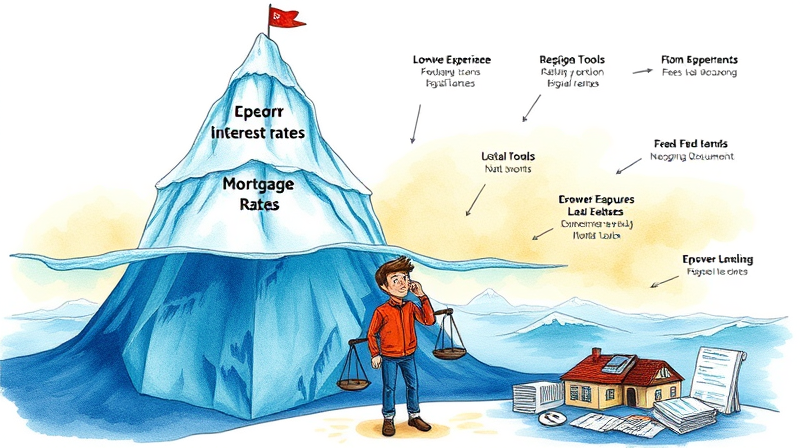

When shopping for a mortgage, the advertised rate is just the tip of the iceberg. Underneath lies a complex network of fees, features, and service factors that can dramatically alter the total cost of borrowing. By exploring every aspect of a loan offer, you empower yourself to make truly informed financial decisions and secure terms that suit your unique needs.

Mortgage rates, such as a 30-year fixed rate at 6.49% (APR 6.64%), grab headlines and dominate comparison tables. Yet these percentages exclude crucial expenses like taxes, third-party fees, and insurance costs. Imagine an iceberg: the visible rate amounts to less than 20% of the picture, while the rest remains submerged and hidden from casual view.

Focusing solely on the rate is like buying a car based on sticker price without considering fuel, insurance, or maintenance. To avoid unpleasant surprises at closing and over decades of payments, you need to dive deeper.

Under the TRID rule, lenders must provide a Loan Estimate within three business days of your application. This document reveals your total upfront fees and projected monthly payments, giving you a fair comparison.

For example, one lender might quote $6,000 in total fees alongside a low rate, while another offers slightly higher fees but a generous lender credit. Only by examining the Loan Estimate line by line can you determine which package delivers the best value.

Not all lenders excel at every loan category. Some firms offer tailored VA loan programs with reduced funding fees, while others focus on jumbo or renovation loans with flexible underwriting. Key categories include:

By matching your needs to a lender’s specialty, you can secure features such as low down payments, waived mortgage insurance, or higher loan-to-value limits that might otherwise be unavailable.

Your personal profile—credit score, down payment size, and debt-to-income ratio—strongly influences the rate and fees you’ll receive. Borrowers with credit scores above 740 often unlock preferred pricing tiers and minimized mortgage insurance, while lower scores can mean higher rates or additional requirements.

Placing a larger down payment can eliminate the need for private mortgage insurance (PMI) and reduce your interest rate. Likewise, some lenders are more forgiving of elevated debt-to-income ratios, allowing you to qualify even when monthly obligations are high.

Beyond dollars and percentages, the application journey itself shapes your experience. Top lenders combine speed and convenience with robust customer support. Key differences include:

A lender might advertise quick approvals but hide a burdensome paperwork process, while another provides a seamless digital interface but slower closing times. Balance your priorities between personalized guidance and technological efficiency.

To truly compare lenders, always gather at least three Loan Estimates and align them by:

Keep your shopping window under 30 days to minimize credit score impact from rate inquiries. This concentrated timeframe allows multiple credit pulls to count as a single inquiry under most scoring models.

Consider long-term cost differences: a $300,000 loan at 4% over 30 years accrues nearly $673,019 in interest due to compounding. Even a 0.25% rate variation can shift your lifetime interest by tens of thousands of dollars.

Federal regulations like TRID ensure transparency, requiring a seven-business-day review period after you receive your Closing Disclosure. This window lets you verify final numbers and lock in credits.

Economic conditions—Inflation trends, unemployment data, and Federal Reserve actions—affect all lenders but prompt some banks to update rates more frequently. Monitor rate sheets daily, and lock in a quoted rate when markets show upward pressure.

Comparing mortgage lenders by more than just the interest rate transforms the home-buying process from a race to the lowest percentage into a strategic evaluation of total value. By dissecting Loan Estimates, matching your profile to lender strengths, and balancing service quality with digital convenience, you position yourself to save thousands over the life of your loan.

Begin by requesting Loan Estimates from three specialized lenders. Review each component, simulate different down payment scenarios, and weigh the trade-offs between fees and rate credits. With this thorough approach, you’ll emerge confident in your decision and ready to secure the mortgage that truly fits your financial goals.

References