Search

Deciding between a secured or unsecured loan can feel overwhelming. Yet, understanding the key distinctions empowers you to make choices that protect your assets and financial wellbeing. In this guide, we explore definitions, risks, benefits, and real-world examples so you can confidently select the right loan for your needs.

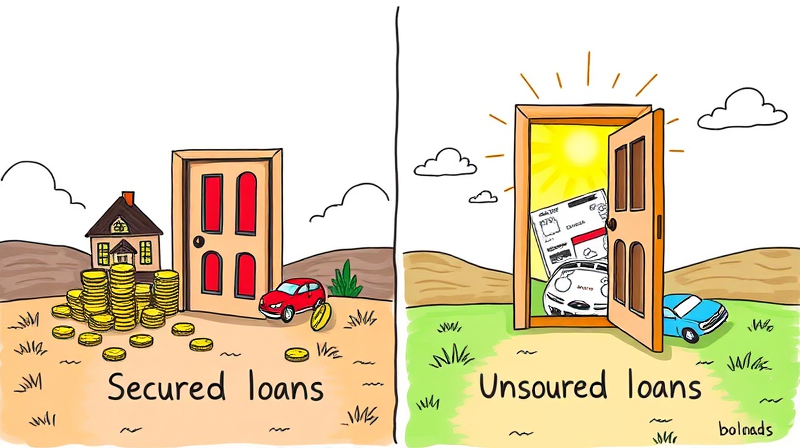

A secured loan requires collateral—a valuable asset you pledge to the lender as a guarantee. Common forms of collateral include houses, cars, savings accounts, or other investments. Because the lender can seize these assets upon default, lenders face reduced risk and often pass savings to borrowers through lower interest rates.

Typical secured loans include mortgages, auto loans, and home equity lines of credit (HELOCs). These financing options allow borrowers to access large sums—sometimes exceeding $100,000—while benefiting from lower interest payments than unsecured alternatives.

In contrast, an unsecured loan does not demand collateral. Instead, lenders rely on your creditworthiness and income history to approve your application. Unsecured loans range from personal loans and credit cards to student loans and lines of credit.

Approval for unsecured financing is often quicker, with many lenders offering online applications and funding within days. However, because there’s no asset to recover on default, interest rates tend to be higher, reflecting the elevated risk lenders assume.

To see how secured and unsecured loans stack up, consider the following table.

Secured loans are generally easier to qualify for if your credit score is fair or poor because collateral lowers the lender’s risk. In many cases, borrowers with scores below 650 can still secure financing, especially if the collateral’s value is high.

Unsecured loans demand stronger credit profiles. To access the most competitive rates—starting around 6.49% APR—you often need a credit score of 690 or above. Borrowers below 689 may face higher rates or outright denial.

Secured loans leverage the value of your asset, enabling you to borrow larger sums with more favorable payment terms. Unsecured loans, while smaller in scale, offer convenience and speed.

Choosing between secured and unsecured loans hinges on your tolerance for risk, credit standing, and urgency. Below are the primary pros and cons to weigh.

Defaulting on a secured loan triggers collateral seizure—your home, vehicle, or other pledged asset can be repossessed. Conversely, an unsecured loan default damages your credit score and may lead to collections or court actions, but your personal property remains intact.

In either case, late payments or defaults remain on your credit report for up to seven years, affecting future financing options.

Consider these typical scenarios:

Your decision should align with your financial profile and borrowing goals. Ask yourself:

If you have sufficient collateral and seek a low APR on a large loan, a secured option is likely ideal. For smaller needs, swift access, and no asset risk, an unsecured loan may be the smarter choice.

Banks, credit unions, and online lenders all offer secured and unsecured options. Major institutions like Wells Fargo, U.S. Bank, and PNC often provide special rates for existing customers. Online platforms, meanwhile, excel at fast unsecured personal loans with minimal paperwork.

Before applying, compare offers, request prequalification to gauge rates without a hard credit pull, and read all terms carefully to avoid hidden fees.

Understanding the nuances between secured and unsecured loans empowers you to choose financing that aligns with your goals. Whether you prioritize low monthly payments, rapid funding, or borrowing flexibility, there’s a solution tailored to your situation.

By evaluating your credit profile, collateral availability, and long-term financial plans, you can navigate the lending landscape with confidence—securing the funds you need while safeguarding your future.

References