Search

The journey of a loan is more than just numbers on a page—it’s a story of trust, responsibility, and financial empowerment. From the first inquiry to the final payoff, every stage matters deeply to both borrowers and lenders.

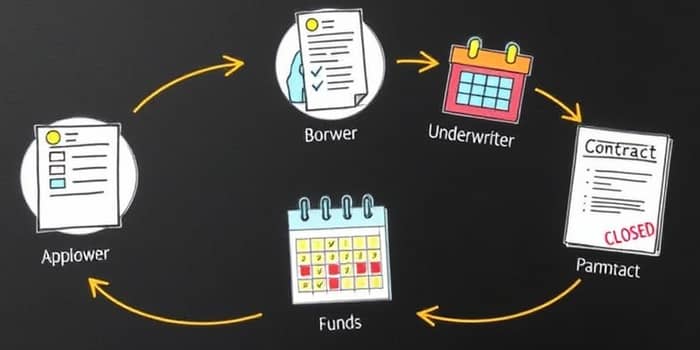

The loan lifecycle, often called the “life of the loan,” is the complete journey of a loan from its initial inquiry through disbursement, ongoing management, and eventual resolution. While some frameworks divide this journey into three broad phases—origination, servicing, and closure—others break it into six or seven detailed steps.

Loan origination encompasses everything that happens before funds move. It begins when a borrower expresses interest and submits an application.

1. Inquiry & Pre-Qualification: The borrower provides basic details—income, employment, desired loan amount—and the lender performs a preliminary credit eligibility check. A soft credit pull and quick debt-to-income calculation help decide if full underwriting is warranted. Successful candidates receive pre-qualification, a nonbinding estimate of loan terms.

2. Application Intake & File Creation: Once pre-qualified, the applicant submits supporting documents and data is entered into a robust digital system. A robust digital loan origination platform creates a centralized loan file that tracks every step, deadline, and compliance checkpoint.

3. Documentation Collection: Requirements vary by loan type but commonly include:

After building the file, lenders verify every claim and analyze risk. Accurate, unbiased assessment is crucial to responsible lending.

4. Verification & Processing: Third parties confirm income, employment, and asset details. Title searches reveal liens on property. Appraisals establish market value. Regulatory checks ensure compliance with consumer protection, fair lending, and anti-money laundering rules.

5. Underwriting & Credit Analysis: Underwriters perform in-depth credit analysis and underwriting to assess the borrower’s ability and willingness to repay. They evaluate credit scores, payment history, debt ratios, collateral value, and overall market conditions for real estate or equipment.

Underwriting outcomes include approval, conditional approval (pending final documents or actions), suspension for additional information, or outright decline. Conditions might require debt pay-off, missing paperwork, or clarifications of credit report items.

With underwriting complete, the loan moves to closing and disbursement, then into long-term account management.

6. Approval, Terms & Documentation: The lender finalizes loan terms—rate, amortization schedule, fees, prepayment penalties—and prepares legal documents: promissory notes, security agreements, deeds of trust. Stakeholder sign-off may include a credit committee, risk officers, and compliance teams.

7. Funding & Disbursement: Funds are transferred to the borrower or to a third party (e.g., escrow for real estate). This moment marks the loan’s official start and the beginning of repayment obligations.

8. Servicing & Repayment: Borrowers fulfill installment payments according to the agreed schedule. Lenders manage accounts using comprehensive repayment tracking and alerts, sending statements, processing payments, adjusting escrow accounts for taxes and insurance, and handling customer inquiries.

Proactive oversight helps reduce defaults and supports healthy repayment behavior.

Lenders perform proactive monitoring of borrower behavior by watching payment patterns and credit updates. Delinquency notices and friendly reminders are issued upon missed payments. If delinquency persists, lenders engage in collections, negotiate workout plans, loan modifications, or refer accounts to recovery agents.

Effective collections balance recovery goals with empathy, maintaining borrower goodwill while safeguarding the lender’s interests.

Every loan reaches an endpoint: full payoff, refinance, charge-off, or legal resolution.

9. Payoff & Settlement: When final payment is made, the lender issues a payoff statement and releases any collateral liens. Borrowers receive confirmation of final closure and recovery processes and certificates of lien release for mortgages or security agreements.

10. Default & Recovery: In cases where loans cannot be repaid, lenders follow established protocols—repossession, foreclosure, legal action, or sale of collateral. Charge-offs are recorded and internal or external recovery teams pursue remaining balances.

Successful loan management relies on efficiency, transparency, and responsible conduct. Key tips include:

By mastering each phase—from swift and respectful collections management to transparent closing procedures—lenders and borrowers can navigate the complex lifecycle of a loan with confidence and trust. Embracing technology, adhering to best practices, and maintaining open communication ensures a smoother journey and healthier financial outcomes for all parties involved.

References